Wealth Management

Accelerate your wealth by starting with less and compound faster. Cut out the middlemen and management fees, and replace the slow wait of passive investing with data-backed swing trading strategies capturing significant market moves in weeks - not years.

The Foundation: Cash Flow

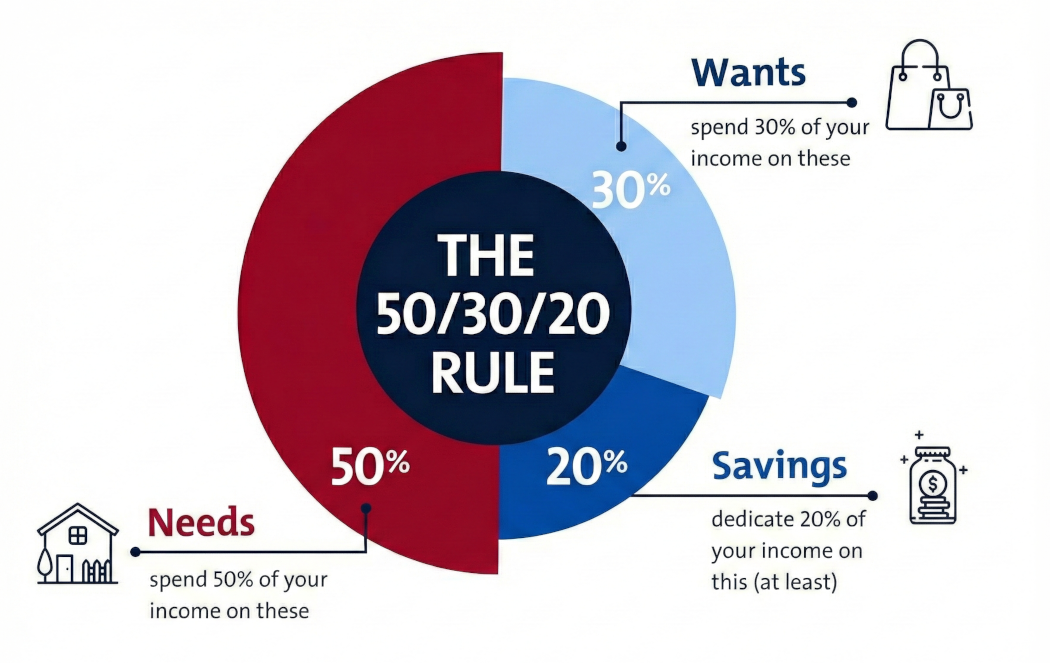

Growing your wealth is all about managing the "gap" between what you earn and what you spend. A simple way to do this is the 50-30-20 rule: use 50% of your income for needs like rent and bills, 30% for things you want, and save the final 20% for your future.

Before you start investing, use that 20% to build a "safety net" of 3 to 6 months of living expenses so you're never forced to sell your investments during an emergency. Finally, focus on paying off high-interest debt first; clearing a credit card with a 20% interest rate is the smartest "investment" you can make, as it's essentially a guaranteed 20% return on your money.

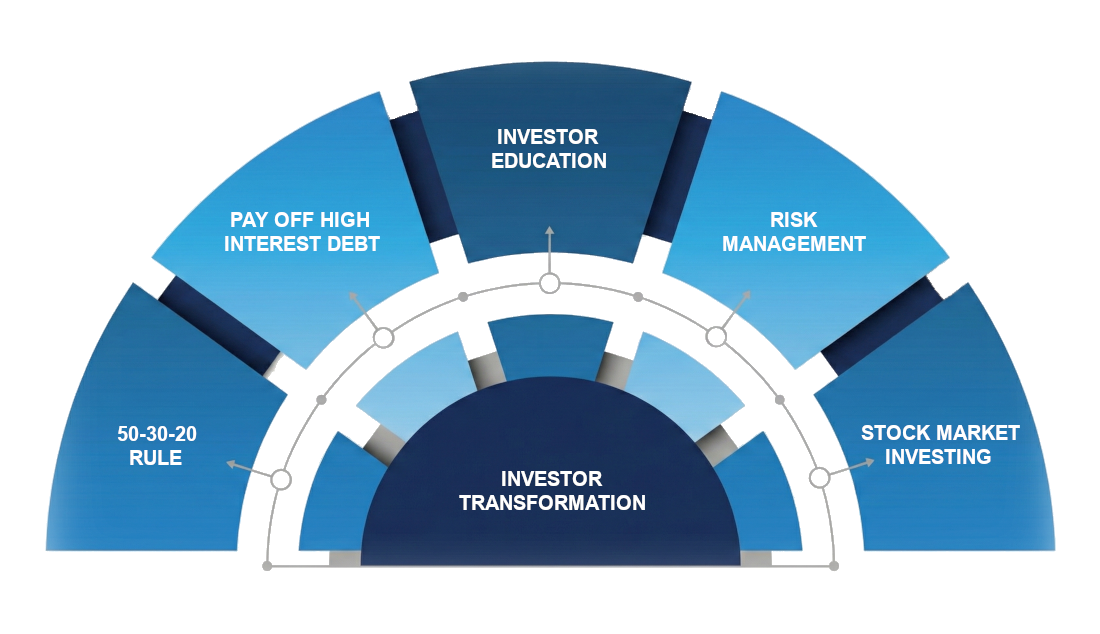

Investor Transformation

It is tempting to jump right in, but the best investment you can make is in your own education. Professional traders aren't gamblers — they are risk managers first.

Before using real money, start by practicing in a "paper trading" account to learn the ropes without any risk. When you are ready to start for real, only use 1% to 2% of your investment savings (that 20% portion of your budget) on any single trade. This disciplined approach protects your hard-earned money while you learn to grow it with confidence.

The Velocity of Your 20%

Think of the 20% you set aside for savings not just as a "safety bucket," but as the fuel for your compounding engine. While passive investing waits years for growth, swing trading puts that capital to work in the short term to create "velocity."

Passive investing is like planting a tree and waiting decades for fruit. Swing trading is like harvesting every few weeks. By identifying stocks ready to move now, you can aim for 5–10% gains in days or weeks rather than waiting a full year. When you consistently reinvest those wins back into your 20% budget, you aren't just saving money—you're accelerating how fast it grows.

If you only grow your 20% through simple savings, it takes years to see a change. If you use swing trading to capture just two or three high-probability moves a month, you change the velocity of your wealth. You aren't working harder for your money; you're making your 20% budget work harder for you.

Higher Frequency

Moving your money through multiple successful trades in a year compounds much faster than leaving it in a single index fund.

The Power of Small Wins

You don't need "home runs." A series of small, data-backed wins on your 20% budget can significantly outpace the traditional 7% annual market return.

Active Compounding

Because swing trading focuses on short-term cycles, you get to "re-apply" your growing capital to new opportunities more often.

The Silent Wealth Eroders

Building wealth is not only about "picking winners", but also about plugging the invisible leaks that quietly drain your capital. While market crashes grab headlines, the true danger lies in two areas: structural costs (like inflation and management fees) that erode your balance automatically, and behavioral mistakes (like loss aversion and anchoring) that sabotage your decision-making.

Mastering your wealth means defending against both the math that works against you and the psychology that leads you astray.

| Wealth Eroder | What Happens | The Trap | The Fix |

|---|---|---|---|

| Inflation | Inflation is the rising cost of living that erodes your purchasing power. If your portfolio returns 7% but inflation is 3%, your "real" growth is only 4%. Holding too much cash is a guaranteed loss. In the current 2026 economy, "safe" money often loses value every day it isn't put to work. Example: Your savings account pays 1% interest, but inflation is 4%. You're losing 3% of your purchasing power every year. $10,000 today will only buy $5,500 worth of goods in 20 years. | Thinking "safe" cash in a savings account is risk-free, rather than a guaranteed loss. | Invest in assets that historically outpace inflation, like stocks, factoring in the hidden tax of inflation. |

| Management Fees | Annual fees charged by mutual funds and advisors compound against you over time. When you pay a 1% fee to a mutual fund manager, you aren't just losing 1% of your money today; you are losing the 30 years of compound growth that 1% would have generated. Example: A 1% annual fee sounds small, but on a $100,000 portfolio over 30 years, it costs you roughly $90,000 in lost growth—nearly one-third of your potential wealth. | Ignoring "small" percentages that quietly compound for decades. | By managing your own portfolio and choosing low-cost index funds or individual stocks, you "earn" that 1% management fee back every single year. |

| Trading Costs | Every buy and sell may incur commissions, spreads, and slippage that create friction. When you move from passive investing to Swing Trading, the "cost" of your portfolio shifts from management fees (which you pay to others) to trading costs (which you control yourself). Example: If you trade frequently and lose 0.5% per round-trip to fees and spreads, making 20 trades a year costs you 10% annually—before any gains or losses. | Over-trading and "churning" your account trying to time every move. | Most major brokerages now offer $0 commissions on US stocks and ETFs, the financial "friction" of trading is at an all-time low. |

| Loss Aversion | Success in swing trading isn't about being a genius; it's about managing your own psychology. Humans feel the pain of a loss twice as strongly as the joy of an equal gain. Professional swing traders don't try to be right 100% of the time; they focus to be profitable across a large number of trades. Example: A swing trader refuses to sell a stock at a $200 loss because the emotional pain of "realizing" the failure feels worse than the risk of holding on. Consequently, they skip their stop-loss and watch that small dip turn into a $2,000 catastrophe as the price continues to plummet. | Letting a "wait and hope" mentality override your trading strategy, and over-confidence causing you to overinvest in a single trade. | Diversify with small positions. Accept that not every trade wins. Stick to your trading strategy. |

| Anchoring | We fixate on the price we paid, refusing to sell until we "get back to even." The market doesn't know or care what price you paid. While you wait for a dead stock to crawl back to your "anchor," you are missing out on other winners. This is the Opportunity Cost trap. Example: You bought a stock at $100, it drops to $60. You hold for years waiting for $100, while that $60 could have grown 50% elsewhere. | Judging an investment by a past price instead of portfolio potential, causing you to miss out on other winners while you wait. | When a 2% position drops, you can cut the loss objectively because you've accepted that they can't all be winners. You are trading a system, not a single stock. |

| Lifestyle Inflation | The subtle process where your standard of living rises to match your increasing income. It is the single most common reason why people who earn a high salary still find themselves "feeling broke" or living paycheck to paycheck. Example: You get a $20,000 raise and immediately upgrade your car payment by $400/month. Your net worth stays flat despite earning more. | Upgrading your lifestyle with every pay increase. | Keep your expenses steady when income grows. Invest the difference in your future. |